Expertise: Gambling Industry Specialist

- The global online casino market has crossed US$145 billion

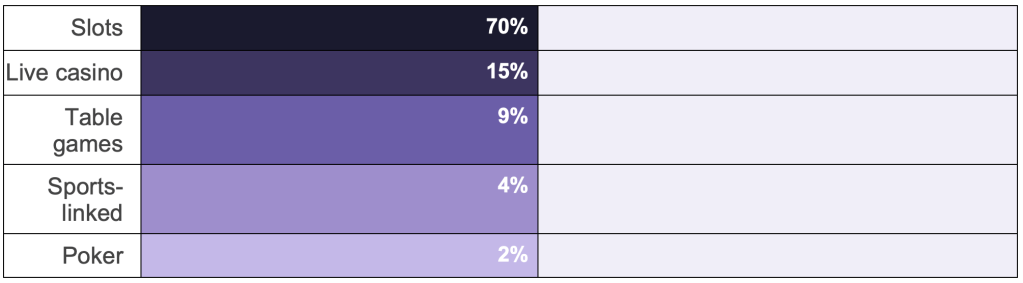

- Slots Dominate 70% of All Activity

| $145B MARKET VALUE | 70% SLOTS SHARE | ~13% ANNUAL GROWTH |

Let’s get the obligatory moment of awe out of the way. One hundred and forty-five billion dollars. That’s the current estimated value of the global online casino market — a figure large enough to dwarf the GDP of dozens of sovereign nations, and yet one that the industry’s more polished spokespeople will tell you is merely a milestone on the way to something considerably larger. They are, almost certainly, correct. And the mechanism driving that ascent is as old as it is simple: the slot machine, now liberated from the carpeted floors of Vegas and transported, with ruthless precision, into the pocket of anyone with a smartphone and a pulse.

“Seventy percent. Not of profit. Not of revenue from whales. Seventy percent of all gambling activity, globally, is people hitting a spin button.”

Seventy percent. Sit with that number. Not of profit. Not of revenue drawn from the highest-spending ‘whales’ the industry so elegantly euphemises. Seventy percent of all online casino activity, worldwide, is a person pressing — or more accurately, tapping — a button that causes symbols to spin and stop. The technological sophistication of a modern video slot, with its cascading reels, volatile bonus features, and mathematically precise return-to-player rates, is genuinely impressive. What is equally impressive, though considerably less celebrated in operator earnings calls, is the psychological architecture underneath it all: variable ratio reinforcement schedules that B.F. Skinner would recognise immediately, wrapped in enough licensed IP and animated penguins to make you forget you are, at core, feeding a machine that is calibrated to return rather less than it receives.

How the pie actually divides

The remaining thirty percent is itself revealing. Live casino — a dealer filmed in a studio somewhere in Riga or Manila, streamed to your screen with millimetre-perfect latency — accounts for the bulk of non-slot activity and is the fastest-growing segment in terms of operator investment. The conceit of the live format is compelling: it re-introduces a human element into what had become a transaction between user and algorithm, lending the proceedings a sense of occasion, of being somewhere. Operators love it because the margins are excellent; players love it because it scratches the social itch of the casino floor without requiring anyone to leave the sofa.

Traditional RNG table games — digital blackjack, roulette, baccarat — occupy a quietly shrinking slice. This is not because they’ve become less mathematically fair; most carry better theoretical RTPs than slots. It is because they demand attention. You must make decisions. You must think, or at least perform the motion of thinking, between each hand. Slots ask nothing of you beyond continued presence. In the attention economy, that is not a small advantage.

Geography, regulation, and the eternal cat-and-mouse

The market is geographically lopsided in ways that tell you more about regulatory history than about human appetite for gambling, which appears to be roughly uniform across cultures and latitudes. Europe remains the largest regulated market, with the United Kingdom, Germany, Sweden, and the Netherlands having variously liberalised, restricted, tightened, and then argued extensively about their frameworks over the past decade. The UK Gambling Commission, for its part, has spent considerable energy developing affordability checks and stake limits that the industry has spent equal energy characterising as existential threats. The Commission has survived this characterisation before.

Asia-Pacific, meanwhile, is simultaneously the most promising and least stable growth frontier. Several of the world’s highest-volume online gambling markets sit in jurisdictions where the legality of online play is, to put it diplomatically, contested. The Philippines has built an entire legal industry — PAGCOR-licensed Philippine Offshore Gaming Operators — around the idea of hosting gambling operations targeting other countries’ citizens. This model is now under extraordinary political pressure from multiple directions, but has proven resilient before. Entrepreneurs in this space have a high tolerance for ambiguity.

“The smartphone didn’t just democratise access to gambling. It liquefied it — making betting as frictionless as checking the weather.“

North America, newly energised by the post-PASPA legalisation wave that began in 2018, remains mostly a sports betting story at the state level, but online casino — iGaming in the industry’s preferred nomenclature — is steadily following in the jurisdictions that have moved first. New Jersey remains the bellwether; Pennsylvania, Michigan, and West Virginia have joined the legal market; and the lobbying apparatus in a half-dozen further states continues its patient work. The numbers from legal US markets are growing with the kind of year-on-year velocity that causes investment analysts to use superlatives without apparent irony.

The technology question nobody is asking loudly

The $145 billion figure arrives as artificial intelligence moves from novelty to infrastructure across the industry. Operators are deploying machine learning not merely for fraud detection — the defensible, press-release-friendly application — but for personalisation at a granularity that would have been impossible five years ago. The question of what it means to have a system that learns, player by player, session by session, exactly which game mechanics generate the longest engagement and the largest deposits, is a question that the industry’s responsible gambling teams are underfunded to answer. It is also, to be fair, a question that regulators are only beginning to formulate correctly.

The smartphone didn’t just democratise access to gambling — it liquefied it. Removed the friction of travel, of cash, of the social signal of walking into a betting shop. An industry that once relied on the slight inconvenience of physical access to create natural breaks in play now operates in an environment where the only barrier between a player and the next session is the phone’s lock screen. The responsible gambling researchers call this ‘structural characteristics of the gambling environment.’ The operators call it ‘seamless user experience.’ They are describing the same thing.

What $145 billion actually means

A market of this scale does not sustain itself on the activity of a small cohort of problem gamblers, as critics sometimes imply, nor on the recreational spending of millions of casual players alone. The truth is messier: it runs on a power-law distribution in which a relatively small percentage of players generate a disproportionate share of revenue, and in which the line between ‘heavy recreational player’ and ‘person experiencing harm’ is one that the industry’s definitions are structurally motivated to locate generously. This is not unique to gambling — it describes the economics of a great many consumer industries — but it is particularly acute when the product’s mechanism of engagement is the variable ratio reinforcement schedule, and when the product is available at three in the morning with no minimum social obligation to stop.

None of this is to suggest that the $145 billion represents only harm. Millions of people gamble online each week without any meaningful negative consequence, and the human appetite for games of chance is ancient and apparently ineradicable. What the number does represent, unambiguously, is leverage — and the question of who holds it, and in whose interest it is exercised, remains the most important one in the industry’s regulatory future. The analysts tracking the growth curve to $200 billion and beyond are correct in their projections. What they model less often is what a market this large, growing this fast, with this much invested in retaining engagement, looks like when the political wind changes.

It will look, the historical record suggests, like a negotiation. It always does. The house, after all, doesn’t just win. It also eventually bargains.