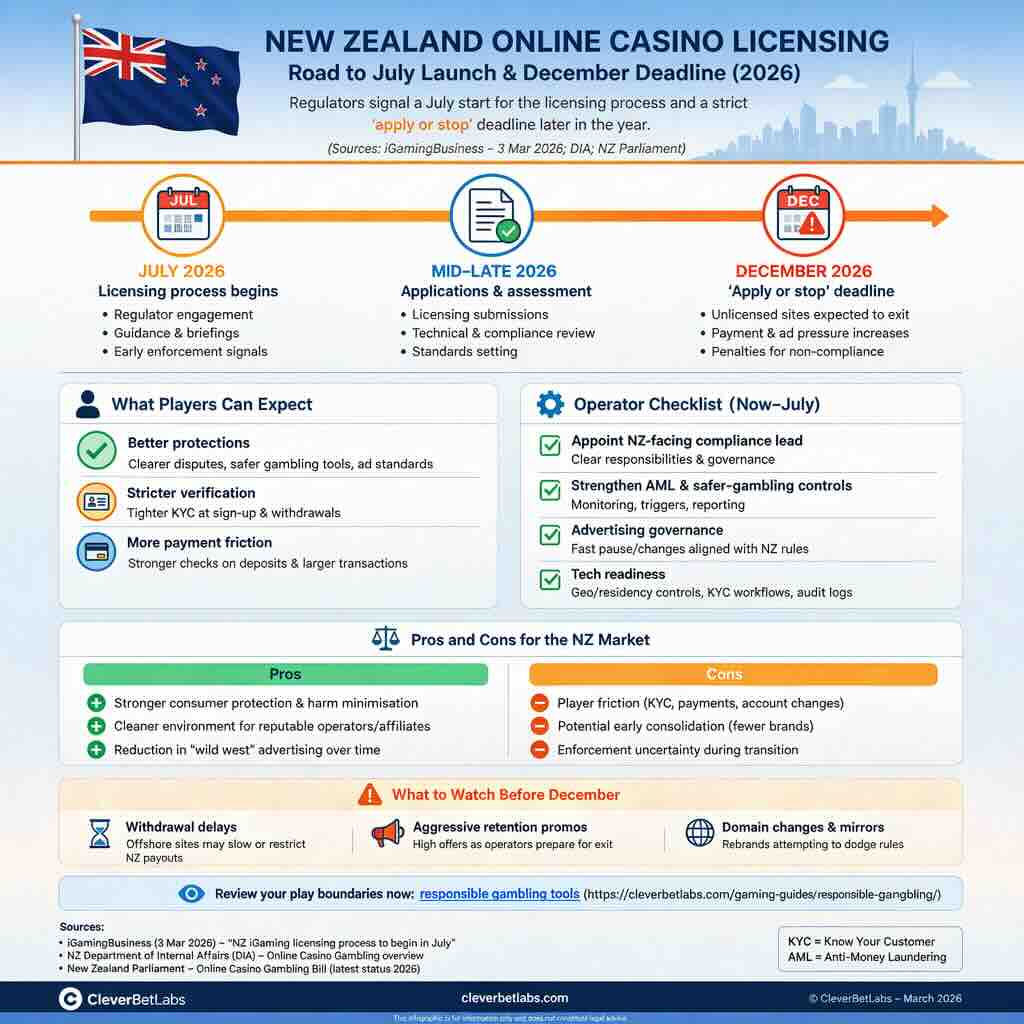

New Zealand’s move toward a regulated online casino market has finally shifted from “policy intent” to a visible timetable: a July 2026 licensing start is now the working target. Officials are framing the reform as a response to the scale of offshore spend and the lack of local oversight. Here, the immediate takeaway for operators is simple: the window to get organised is no longer theoretical. For players, the bigger change is what happens when the market flips from today’s largely offshore environment to one where access, advertising, and player protections are anchored in a domestic framework.

The March 4 report from SiGMA is explicit about the direction of travel. The Department of Internal Affairs (DIA) has published an outline of how the licensing process would unfold once the Online Casino Gambling Bill becomes law, with the government “planning to begin its licensing process in July 2026.” It is recommended that players stick to well established online platforms that have secure payment transfers.

Why the urgency now?

Part of the political argument is money leaving the country. SiGMA cites government estimates that New Zealanders spend more than NZ$750 million per year on offshore online casinos. Spend that currently sits outside New Zealand’s regulatory perimeter. It simply doesn’t contribute to local tax or community funding in the way land-based gambling does. That’s a big number, and it frames the bill less as a niche reform and more as a market capture and consumer-protection exercise.

What’s also clear is that licensing won’t be “one form, one approval.” The DIA outline (as described in the March 4 reporting) sets a three-stage process, and a market cap of 15 operators. Stage one is an expressions-of-interest phase expected to run for one to two months, allowing prospective licensees to put their hands up and begin the suitability journey. The later phases escalate from signalling to competition and scrutiny.

Even with a July start target, the bill’s parliamentary passage matters. SiGMA notes the bill passed its first reading in July 2025 but still must clear the remaining stages before it can be enacted. In other words: July is presented as the intended start for the licensing process, but the timeline is still gated by legislative progress. That distinction matters for operators planning budgets and for affiliates assessing when a “regulated-only” environment actually begins.

What are the current market dynamics?

The market design, however, is already being discussed in practical terms: up to 15 operators, a staged entry mechanism, and a licensing system that is supposed to bring offshore play under a domestic harm-minimisation umbrella. That’s the official story: channel activity into a monitored system with stronger protections for players.

For operators, the most underestimated risk isn’t “getting rejected.” It’s getting slowed down. A staged process tends to reward teams that can submit clean documentation and respond fast when the regulator asks for clarifications. In a capped market, delays can become competitive disadvantages because regulators usually run in batches and prefer comparable assessment windows. If you miss a documentation beat early, you can find yourself stuck behind the pack even if your brand is strong.

There’s also a second-order effect: a licensing timeline changes how upstream partners behave. Payment providers, ad platforms, and media publishers become more cautious when a market signals it’s heading to “licensed-only” operation. That’s not about morality—it’s about risk. If enforcement language hardens (or even if it’s merely implied), partners will start asking “are you in the licensing queue?” before they agree to integration or promotion. The moment government and DIA talk in timelines, market infrastructure adjusts.

For affiliates, this is where content strategy gets real. When licensing systems switch on, the sites that win are rarely the ones that scream the loudest. They’re the ones that can explain, calmly and credibly, what the reform means to players and how to spot legitimate operators as the market transitions.

What should players expect in the near future?

For players, the likely shifts are predictable:

- Verification friction increases. Regulated markets tend to demand more robust identity checks and cleaner payment trails. That can feel annoying but reduces the “vanish and never pay” risks that dominate offshore complaints.

- Advertising becomes more formal. Licenced operators can often advertise more openly, but the regulator usually sets guardrails around targeting, claims, and responsible messaging.

- The menu of choices can narrow at first. A capped system plus compliance costs often means fewer brands early, even if the game library remains broad within licensed platforms.

One area you can expect regulators to push hard is harm minimisation—not just as a slogan, but as a measurable requirement. That can include deposit limits, time-outs, self-exclusion tools, and more proactive customer interactions when risk indicators spike. If you want a player-friendly explainer page to route readers to, point them to responsible gambling.

New era for operators

From the operator side, July is effectively the moment the “pre-application sprint” ends and the “compliance marathon” begins. If you’re serious about this market, you need at minimum:

- A clear compliance ownership structure (who is responsible, who signs off, who answers regulators)

- A documented safer gambling framework (tools, triggers, interventions, escalation)

- A marketing governance plan (how you ensure affiliates and partners comply)

- A data and reporting capability that can satisfy audit expectations

The upside is equally clear. If New Zealand succeeds, it becomes a more stable environment for high-integrity operators and for consumers who want predictable protections. The downside is that any market change creates transition pain: slower withdrawals at some sites, confusing rebrands, and friction while systems “learn” each other.

The key signal from March 4 is that New Zealand now has a publicised direction and a target start. That alone changes how the industry behaves. In iGaming, timelines are power. And New Zealand is now putting dates on the board.

Sources

SiGMA, “New Zealand plans July start for online casino licence applications,” March 4, 2026.